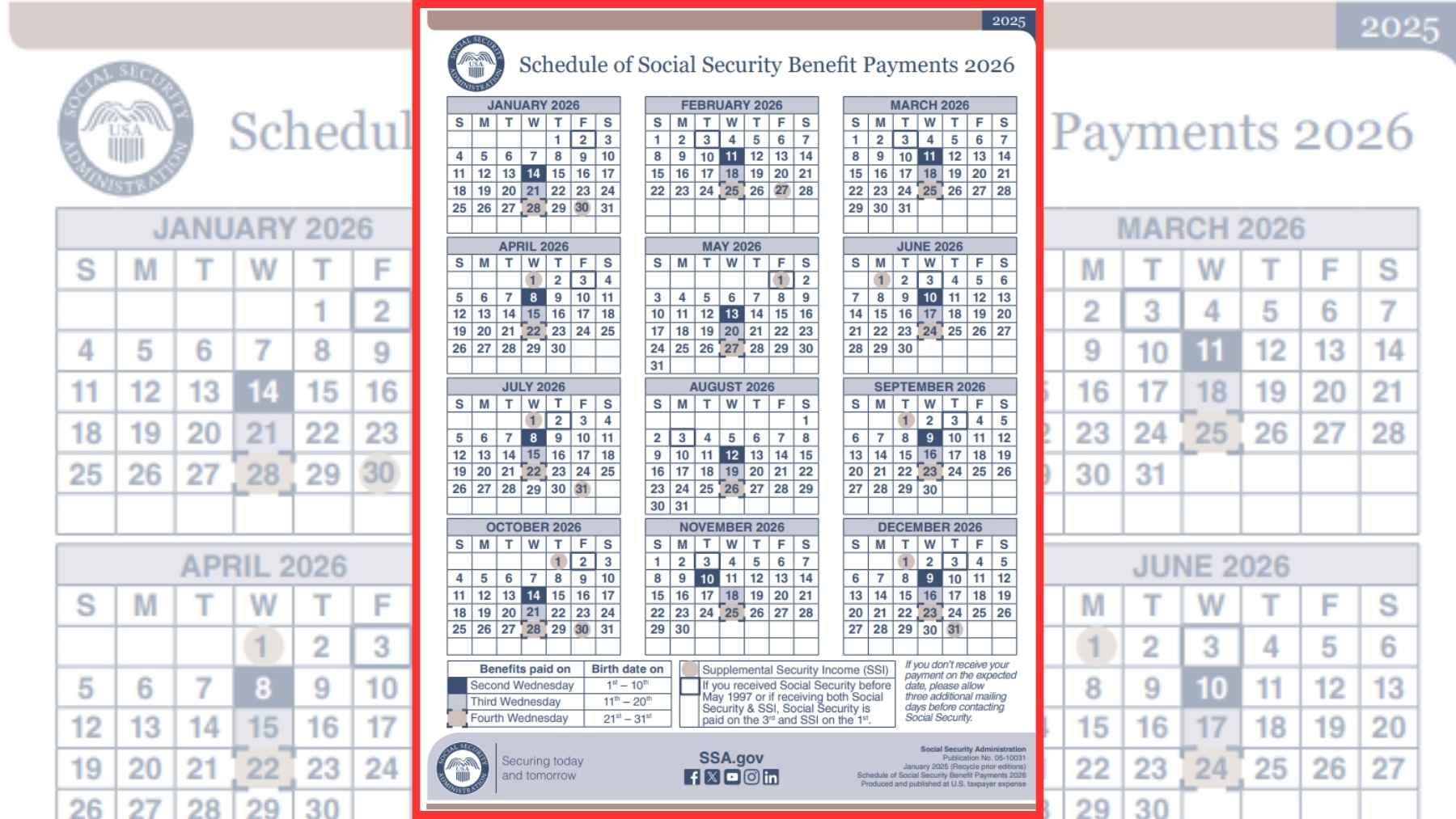

Essentially, many citizens of the United States’ Social Security benefits are, in a way, regarded as a means of funding for their retirement. While the starting age for collecting benefits influences the monthly payment size, a frequently neglected strategy can significantly increase these benefits in the long run. It also increases the number of credits that can be collected and expands the monthly income stream when the claim is filed later.

That’s why the proposed legislation regarding work after the retirement age is insufficient to improve the situation: delayed retirement credits. Through this knowledge, one could significantly increase the monthly social security income, thus ensuring a more settled retirement period.

Understanding Delayed Retirement Credits

The delayed retirement credits are the form of Social Security payment increase that the Social Security Administration (SSA) provides for extending the period beyond the full retirement age (FRA) without claiming the Social Security retirement benefits. Suppose you start receiving your benefits early before reaching your full retirement age between 66 and 67.

In that case, your monthly benefits are reduced by a fixed percentage for every year of early receipt of benefit and on the other side, for each year you postpone your benefits after your full retirement age up to the age of 70, your monthly benefits are adjusted again by a fixed percentage. It is called the delayed retirement credit, which today equals 8% of the year or two-thirds of 1% for a month. Such decisions allow you to obtain these credits placed on top of your base, thus securing a higher monthly amount for your whole life once you begin receiving your payments.

Quantification of the Potential Increase

Reducing the retirement age also affects how much money Social Security pays an individual monthly. For example, if your full retirement age is 67 and you opt for delayed retirement benefits at 70, you will receive 24 per cent more than if you had filed for benefits at 67. This increase can mean hundreds of dollars a month, which is especially relevant in the context of retirement plans.

Besides, the longer you live, the more you will be oriented on the higher monthly payments and, perhaps, will receive an impressive sum of money during a whole life span. These higher payments are cumulative, meaning the additional income could be tens of thousands of dollars throughout retirement.

Strategies for Maximizing the Benefits

As mentioned earlier, delaying receiving retirement benefits may not always be possible. Nonetheless, there exist ways that you can use to leverage delayed retirement credits. Some strategies include looking for work, perhaps working part-time while having other sources of personal income until 70 or retirement age.

It gives you more time to acquire as many credits as possible, thus resulting in a higher monthly payment for the rest of your lifetime when you elect to take Social Security benefits later. Another strategy is coordinating with a spouse or a partner: one of the spouses takes the benefits at the FRA while the other waits, thus receiving some income while earning the maximized delayed retirement credits simultaneously.

Boost Your Retirement Income with Smart Planning

Delayed retirement credit strategy thus presents a good chance to maximize your Social Security benefits and improve your financial wealth in retirement. Therefore, by knowing more about this strategy and how it is possible to improve it, you can have a higher chance to double your monthly income and, therefore, have a good life after working years.

The same applies to all the financial decisions one makes, so one must look at one’s situation, retirement plans, and overall financial capacity before making this decision. Thus, the delayed retirement credit strategy is useful for individuals who postpone receiving benefits for a longer period, as it will positively affect their financial situation in the future. For the best approach to optimize their options, it is recommended to seek the assistance of a financial planner or a specialist in Social Security benefits.